Adopting innovative technology – Digital ID Systems

Those of us who’ve worked in financial services for years know that the levels of regulatory compliance keep rising, no matter where you sit in the investment lifecycle. It’s something we need to do, so we take steps to meet the various requirements, taking whatever risk-based approach we’ve chosen for our business with diligence, often without thinking about the consequences for other stakeholders.

I encountered an example of this when I opened bank accounts when I moved to Jersey in the Channel Islands. I selected the International side of my UK bank, naively assuming that given I’d been a client for 20 years, it would make the process simple in Jersey. Not quite. They are two separate legal entities, I was reminded, and the International one had to do their own due diligence. Could I please bring in my passport with a photocopy, duly certified by someone on island who had known me at least 2 years. And a certified copy of a utility bill to prove my address. Ok. No problem right? I’d only moved to Jersey the previous week and knew very few people who were permitted to certify document, and fewer who’d known me long enough to meet the criteria. Fortunately, I was able to get the passport suitably certified. I also hadn’t received a first utility bill because I had only just set up my accounts with the utility’s providers. I had to call one of them to ask if they would be willing to produce an account statement for the account despite not even having a first reading to give them. They seemed used to this request, which surprised me, and cheerfully produced the required statement for me. I then headed to the bank for my in-person appointment, clutching certified copies and originals, and the multi-page application forms that had to be completed and signed in ink.

That must have been years ago, right? Nope – within the past 4 years. I went through the same process setting up my first Jersey company. I had to go in person to the company’s registry with original and certified documents and application forms, signed in ink. The team there were great, walked me through the process and sent me off with my original documents in a matter of minutes. No worrying about original documents getting lost in the post when you go in person to set up a company.

Scroll forward past the pandemic. Have either of those scenarios changed? Setting up a company certainly has. The JFSC has an on-line system now which guides you through the process and enables you to submit all the documents electronically. If there are problems with the submission, they email you back and guide you through what needs to be changed so you can resubmit the document. When I set up Phundex during the early days of the pandemic, working remotely and online was all new, but the company registry team made it all much easier, and I didn’t have to head down in person. I suspect it was easier because I’d already set up a first company in person, but the system is much more streamlined now. Setting up a bank account? Not so much.

While I understand each organisation must meet their due diligence requirements, it makes no sense to have customers (corporate or individual), having to provide differing levels of due diligence information to multiple organisations for the same transaction. For example, trust administrators do their due diligence to set up trusts for clients, and then those clients must go through an entirely different process with the banks to get bank accounts set up. How frustrating for those customers!

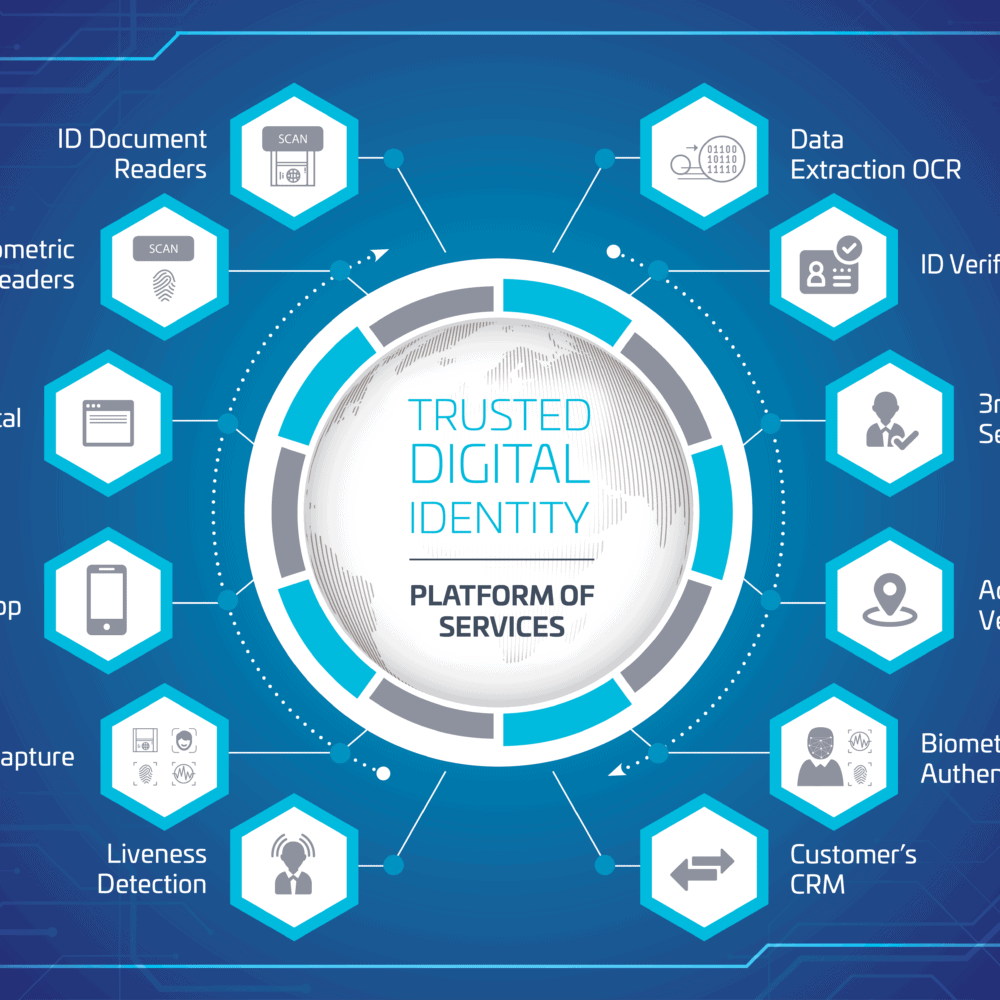

How can we solve this? It’s a time consuming and manually labour-intensive process, which is being replicated every day across the industry. Adopting technology such as Digital ID Systems can go a long way to streamlining the process, improving colleague and customer experiences. There are lots of options out there. So why aren’t more financial services businesses using them?

In the innovation meeting we attended regarding the current Digital ID Systems consultation, the Government and the JFSC clearly encouraged regulated firms to use technology to improve their overall regulatory compliance. They also pointed out that FAFT and Moneval support and promote adopting technology to enable a firm’s comprehensive regulatory framework.

The JFSC consultation paper on Digital ID Systems tells us the three main barriers to adoption are:

Lack of industry confidence to invest in digital solutions

how do they really work/how do I assess them/know they do what they say they do

Differing risk appetites across businesses and sectors

Internal risk appetites across sectors and client types drive differing internal requirements for the same clients in different organisations

Lack of critical mass uptake

who wants to risk the first mover disadvantage of getting it wrong

The consultation is proposing three options to address some of these barriers:

Further clarification in the existing regulatory regime, enhancing Section 4 of the AML/CTF Handbook and incorporating Digital ID Systems into law

Establish an accreditation framework in which Digital ID Systems and their providers are accredited

Create new class of regulated business so that Digital ID Systems Providers become Supervised Persons regulated by the JFSC

Phundex is neither a Digital ID Systems Provider, nor a Supervised Person, so we’ll stick our head above the parapet. Option 1, in our view, must happen. But there also needs to be consistent application of the regime amongst the Supervisors, and an open dialogue between Supervisors and Supervised Persons on the use of technology and how it supports regulatory requirements within a Supervised Persons’ Risk Framework.

Option 2 is a good idea and one we fully support. The Digital ID Systems Providers we know would be willing to get accredited to help clients be comfortable with using the technology as part of their overall process. Unfortunately, its not a quick solution to work out an accreditation regime, get accreditors and start the process, but we’ve got an opportunity to push for clarity and make it easier for digital adoption by Supervised Persons.

Option 3 is unlikely to work. While Jersey based Digital ID Solution Providers might consider it, those based outside Jersey are unlikely to want to become subject to its regulatory regimes, nor are they being asked to in most other jurisdictions. Requiring this would likely reduce the number of options available to Supervised Persons, defeating the global nature of our industry in Jersey, and the purpose of this consultation.

What are your thoughts? This is your opportunity to provide feedback on the consultation “Facilitating the Adoption of Digital ID Systems”. Comments are due by 31st August 2022, so if you haven’t submitted yours yet, there is still time. Jersey Finance is coordinating an industry response, so if you prefer to be part of the industry response, email Nathalie Andersson nathalie.andersson@jerseyfinance.je who is coordinating the response.

You can find more articles on our website, at Phundex Resources, on LinkedIn at Phundex LinkedIn, or for other questions, please email us at: hello@phundex.com.

To book a demo or do a trial, you can either use the link on our website or email support@phundex.com and they will be happy to set it up for you.